July Sale!

July Sale!

Trump accounts are brand new. They just launched on July 4th, 2026. I opened one this week and wanted to share what I found. I’ll start by saying I’m pretty offended by Trump slapping his name on everything (see the Kennedy Center), but I wanted to give these a fair review without being biased by the name on the account. To give credit where it’s due, opening the account was easy and the interface is really nice. My account was approved for my one year old in about an hour. The $1,000 initial deposit from the Treasury says it’s still on its way and will take about a week.

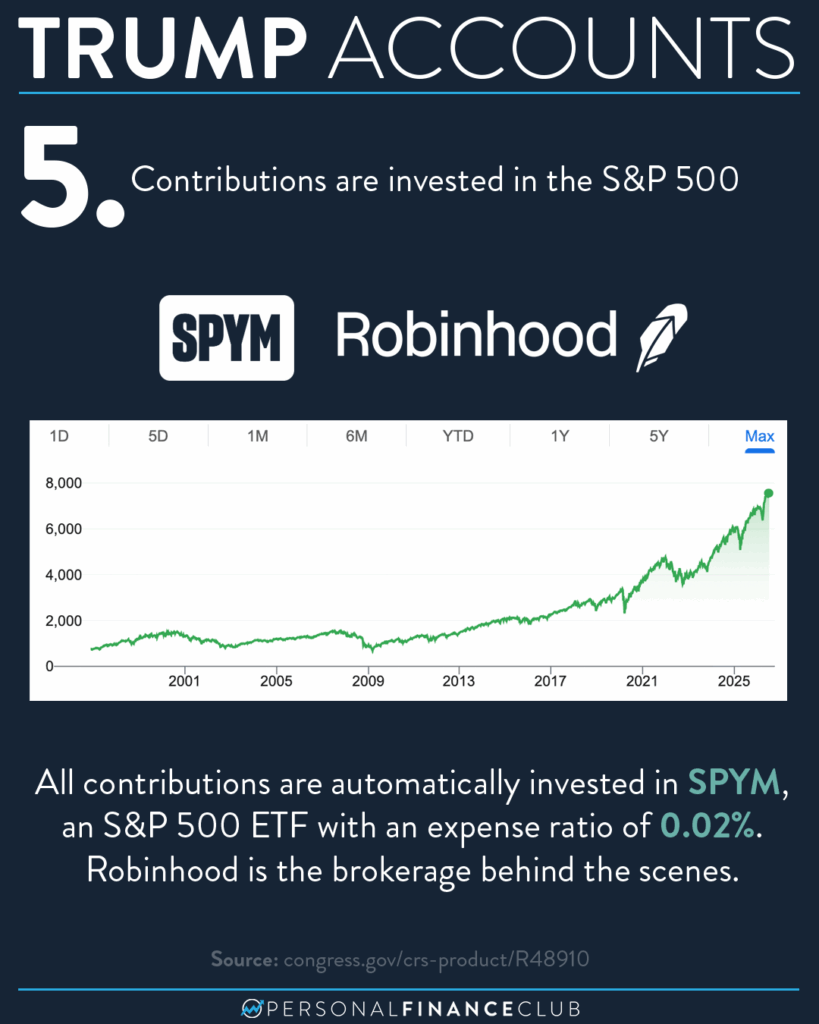

I dug as hard as I could to find any other sort of hidden fees (beyond the transparently advertised 0.02% expense ratio on SPYM) and I couldn’t find any. I believe Robinhood is being paid by a government contract (our tax dollars) as opposed to charging us fees directly.

I’m going to keep an eye on this account to see if anything unexpected happens. For now, my general strategy for investing for my kids is as follows:

• 529s: Well funded to pay for college

• UGMA/UTMA: Any birthday/gift money goes here, invested 60/40 in US/International index funds. The kids will get that money when they turn 18, along with a lesson on financial discipline.

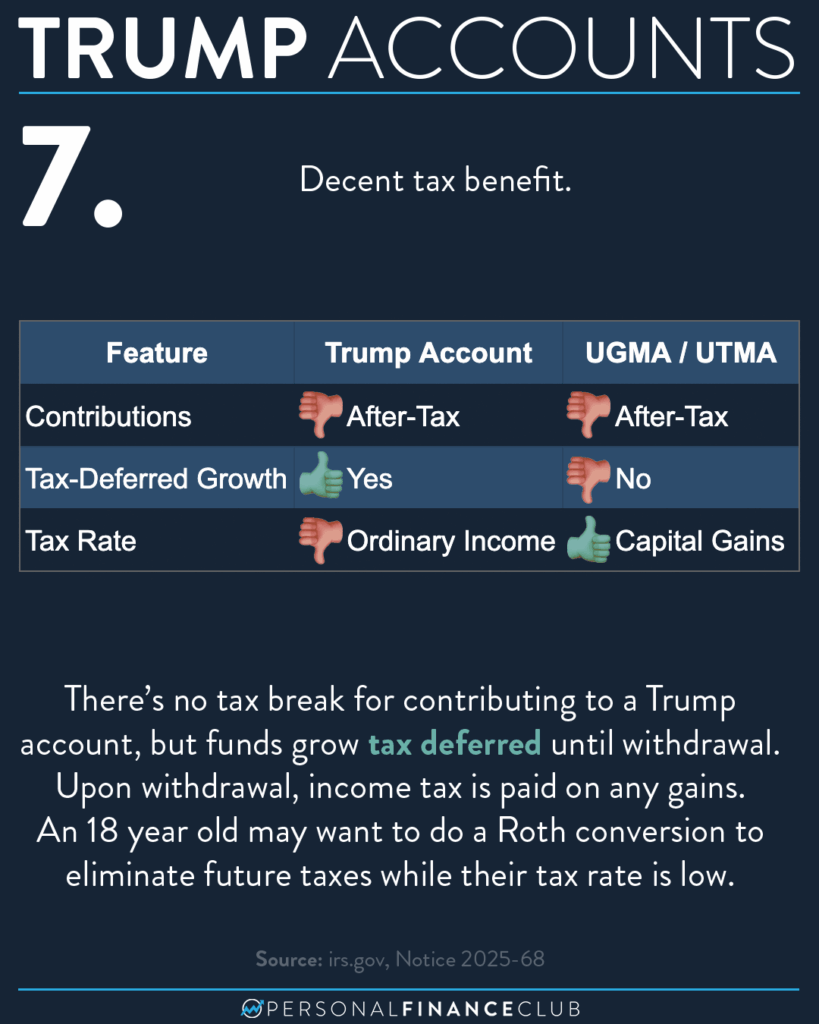

• Trump Account: Just the $1,000 initial deposit from the Treasury for now, but I could see putting gift money here (with a plan to convert to Roth at 18) if I wanted to focus on funding the kids retirement.

• All other money: Goes into OUR trust account. Because our kids aren’t rich, WE’RE rich. We can always GIFT them money later, but beyond the above, I don’t see a reason to funnel money into my kid’s names. I want them to learn to work and build their own futures and fortunes.

Have you opened a Trump account yet? Do you plan to?

As always, reminding you to build wealth by following the two PFC rules: 1.) Live below your means and 2.) Invest early and often.

-Jeremy