September Sale!

September Sale! The quick answer

It doesn’t matter because you shouldn’t be holding cash in your Roth IRA anyway. So just pick SPAXX and go on with your life.

Longer explanation

If you’re using Fidelity, you might see a button like this:

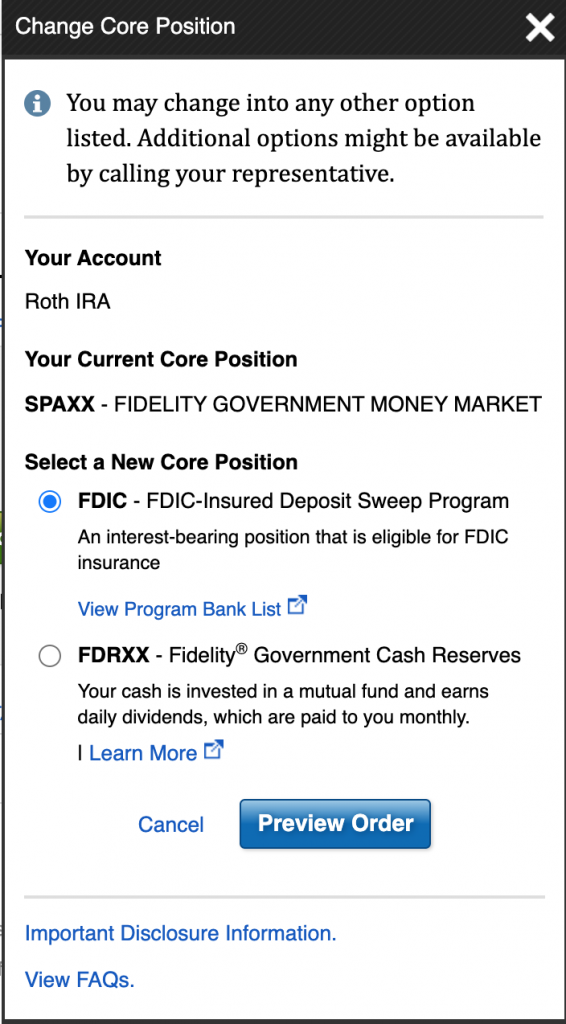

That looks tempting, so you click on it and see something like this:

So you have some options! Let’s break it down.

What is a “core position”?

When you open an investment account, like brokerage account or a Roth IRA the idea is that you put money into the account then use that money to buy investments (like mutual funds, ETFs, stocks, etc). But when there is money in there that hasn’t been used yet to buy an investment, it sits in the “core position”. Which is basically just cash sitting there, like a savings account. Since Fidelity is a full featured brokerage, they give you a few different ways to hold the cash. That’s what this choice is all about.

Why this doesn’t matter!

Since the point of an investment account is to invest, you generally shouldn’t have money just sitting around in cash. This is especially true for young people inside of a retirement account like a Roth IRA. If you have money sitting in your core position in your Roth IRA, you’re likely making a big mistake. You want to invest that money in something like a target date index fund. And since you’ll have no money in your core position, it doesn’t really matter what your core position is! That said, let’s break it down anyway.